The Westminster parties’ attacks on full fiscal responsibility (FFR) for Scotland and the IFS figures being presented unchallenged in the metropolitan media are so fundamentally flawed it is difficult to know where to start. Going back to fundamentals its worth remembering the whole point of a national economy is to create prosperity and security for the population and definitely not to grow the economy for the sole benefit of the financial markets.

The Westminster parties’ attacks on full fiscal responsibility (FFR) for Scotland and the IFS figures being presented unchallenged in the metropolitan media are so fundamentally flawed it is difficult to know where to start. Going back to fundamentals its worth remembering the whole point of a national economy is to create prosperity and security for the population and definitely not to grow the economy for the sole benefit of the financial markets.

Running a deficit is entirely proper, entirely necessary to protect businesses and people and to boost economic recovery after an economic crisis. When you operate a large deficit, over time you do need to reduce that deficit as a percentage of GDP. The argument in this election is over the speed of deficit reduction as a percentage of GDP. It is about finding the optimum balance between economic growth and social protection. If the people of Scotland thought running a larger deficit than the UK was such a bad thing then the Conservatives would be sitting on 49% in the polls, not the SNP.

The media use of colourful and entirely negative language in headlines is also very telling as scaremongering tactics are only deployed when you have no positive case to make. For example, to label an additional £7.6bn deficit (a highly disputed figure) as a blackhole demands an urgent policy reaction involving cuts or tax rises. However, if the front pages were to say that Scotland had committed to “£7.6 billion of prosperity and social protection borrowing” over and above the UK levels, then people might reasonably expect that borrowing to be paid down over a socially and economically responsible timeframe. For example, the IFS forecast being touted as bad news for Scotland actually predicts Scotland’s economy will grow by fourteen thousand million pounds between now and 2020 and this means that Scotland’s nominal deficit will reduce year on year as a percentage of GDP from 8.6% in 2015-16 to 4.6% of GDP in 2020. So the deficit is nowhere near the size of a problem as we have been led to believe by the scaremongering.

If the goal of slower managed deficit reduction is aimed at social protection and stimulation of medium-term economic growth, then the slower paying down of the deficit does not create a blackhole but is sensible and responsible plan. However, that takes us to the second problem with the IFS’s Scottish deficit predictions and that is that the calculations are fundamentally flawed. The IFS admits that its five year reduction as a percentage of GDP does not take into account any additional growth in Scotland’s economy due to the impact of applying bespoke economic policies aimed at creating additional economic growth.Their rationale for not forecasting additional growth from FFR is that measures such as cuts to corporation tax and air passenger duty would, at least in the short to medium run, cost the government money and hence could widen rather than shrink the fiscal gap, even if they did boost growth.

This again is flawed thinking, there are ways around this, firstly as championed by Business for Scotland the 3% blanket corporation tax cut has been replaced by a plan to offer targeted tax cuts based on growth related business investments. For example, if a company qualified for a tax rebate as a result of increasing productivity, employing more people or generating significant export growth then the additional tax revenues from new jobs created, the lowering of demand for welfare, new export duties and additional taxation on sales such as VAT would all be collected before the rebate was due. This could largely offset the impact of such measures on the fiscal gap as well as creating additional revenues for the following year to build upon, thus increasing the revenue baseline improving the following years fiscal position.

Another big issue with the credibility of the IFS figures is that they seem to assume that oil prices won’t recover for five years. Frankly that is finger in the air economics and ridiculous. They predict North Sea revenues will average £0.7 billion a year till 2020, rather than the £2.6 billion a year it forecasted earlier this year. The mistake here is in not including several scenarios, one of which would include oil prices rising. Oil prices are incredibly difficult to forecast right now as the reason for the fall is geopolitical rather than structural. Increasing demand for oil, especially from developing Asian economies, is causing natural upward pressure on oil prices but every time that takes effect the Saudis open the taps to keep it artificially low, partly to punish America for not being aggressive enough with ISIS, to slow Americas shale oil production and to punish Russia for supporting Saudi Arabia’s opponents in the gulf. A return to normal levels of instability in the Middle East versus the current chaos, could change OPEC policy and see the price skyrocket, possibly generating a Scottish revenue surplus before the rest of the UK.

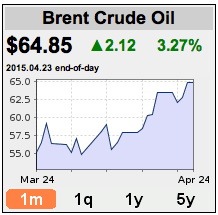

It is worth noting that Brent crude hit $64.85 a barrel today, up 40% from its January low of $45 and that the price of oil has fallen by 50% five times in the last 30 years. So what is happening now is natural volatility and only a major problem for countries without the foresight to create a sovereign oil fund when the price was high. Tony Hayward, the former BP chief executive, said on Tuesday that oil prices are set to soar as Opec has taken just six months to stop the US shale oil boom in its tracks. Hayward said “Opec had shown itself to be the most successful cartel in history” and predicted oil prices would soon return to near $80 a barrel.

It is worth noting that Brent crude hit $64.85 a barrel today, up 40% from its January low of $45 and that the price of oil has fallen by 50% five times in the last 30 years. So what is happening now is natural volatility and only a major problem for countries without the foresight to create a sovereign oil fund when the price was high. Tony Hayward, the former BP chief executive, said on Tuesday that oil prices are set to soar as Opec has taken just six months to stop the US shale oil boom in its tracks. Hayward said “Opec had shown itself to be the most successful cartel in history” and predicted oil prices would soon return to near $80 a barrel.

The goal of Full Fiscal Responsibility is to find the right balance between economic growth, social protection and deficit reduction. In contrast, Westminster’s ill-considered austerity consensus represents full financial irresponsibility.

Business for Scotland – Prosperity for Scotland – Join us now

It’s an demonstration of just how biased the metropolitan mainstream media has become that the microeconomic analysis of the IFS gets held aloft in such high esteem, is portrayed as factual and authoritative and is presented as being above and beyond criticism. One only needs to look at the forecasts of the OBR and UK treasury in 2010 and 2011 to realise that economic forecasts are notoriously inaccurate and, more often than not, heavily influenced by ideological bias and other agendas.

If you were to ask a Keynesian economist for a macroeconomic analysis of the future prospects of the Scottish economy they would come up with a completely different answer from the IFS.

Keynesian economics was replaced by Neoliberal economic theory, as espoused by Milton Friedman, Margaret Thatcher, General Pinochet, Ronald Regan and others, in the 70s and 80s. The experiment has demonstrably failed. The idea that wealth would trickle down has not been reflected in reality.

According to Wikipedia; “Based on their assessments of the extent to which what she describes as neoliberal policies contributed to income disparities and inequality, both [Naomi] Klein and Noam Chomsky have suggested that the primary role of what they describe as neoliberalism was as an ideological cover for capital accumulation by multinational corporations.” (Source;

https://en.wikipedia.org/wiki/Milton_Friedman )

Arguably (economists from opposing sides of this debate couldn’t agree on the colour of poo) it was excessively Neoliberal policies that led to the great depression in the 1930s and caused the financial crash in 2007/8. It caused the de-industrialisation of the UK in the 80s and 90s and has caused the most unequal sharing of the UK’s wealth seen since Dickensian times.

Nicola Sturgeon has challenged the Neoliberal consensus and is quite right to do so. The Financial Times acknowledged the merits of her approach as do many esteemed economists but for as long as most of the mainstream media is owned and controlled by a Neoliberal elite, any challenges to the validity of the Neoliberal consensus will continue to attract limited coverage.

Almost every time the IFS is mentioned by the mainstream media or politicians it is prefixed with the word “independent” but just how independent and competent is the IFS?

The IFS is indirectly funded by Vince Cable’s Department for Business Innovation and Skills via a non departmental public body (NDPB) called the Economic and Social Research Council (ESRC). Could this be a case of “he who pays the piper calls the tune”?

According to their website; “Today, IFS is Britain’s leading independent MICROeconomic [my emphasis] research institute. Its research remit is one of the broadest in public policy analysis, covering subjects from tax and benefits to education policy, from labour supply to corporate taxation.” (Source; http://www.ifs.org.uk/about/)

Notice that the IFS specialises in MICROeconomics and not MACROeconomics. “The difference between micro and macro economics is simple. Microeconomics is the study of economics at an individual, group or company level. Macroeconomics, on the other hand, is the study of a national economy as a whole. Microeconomics focuses on issues that affect individuals and companies.” (Source; https://blog.udemy.com/difference-between-micro-and-macro-economics/)

It is at least questionable whether the IFS are properly qualified and experienced to comment on the MACROeconomic implications of government policies. As demonstrated in this Business for Scotland article, IFS reports consistently fails to take account of MACROeconomic factors. Instead, and unsurprisingly based on its CV, it focuses its attention on MICROeconomic factors. At best, their assessments of the future economic performance of the Scottish economy could be incomplete and at worst they could be significantly misleading.

So, in summary, the IFS is funded by the ESRC which is a NDPB that is funded by Vince Cable’s Department for Business Innovation and Skills. The IFS specialises in microeconomics, not macroeconomics.

There’s a real lack of appetite for dissecting this in the Scots media, allowing the unionists to make hay with project fear the sequel. Thanks for setting this right.